AI

Flex Expands Cerebras AI Production Sevenfold as a Spin-Off Looms

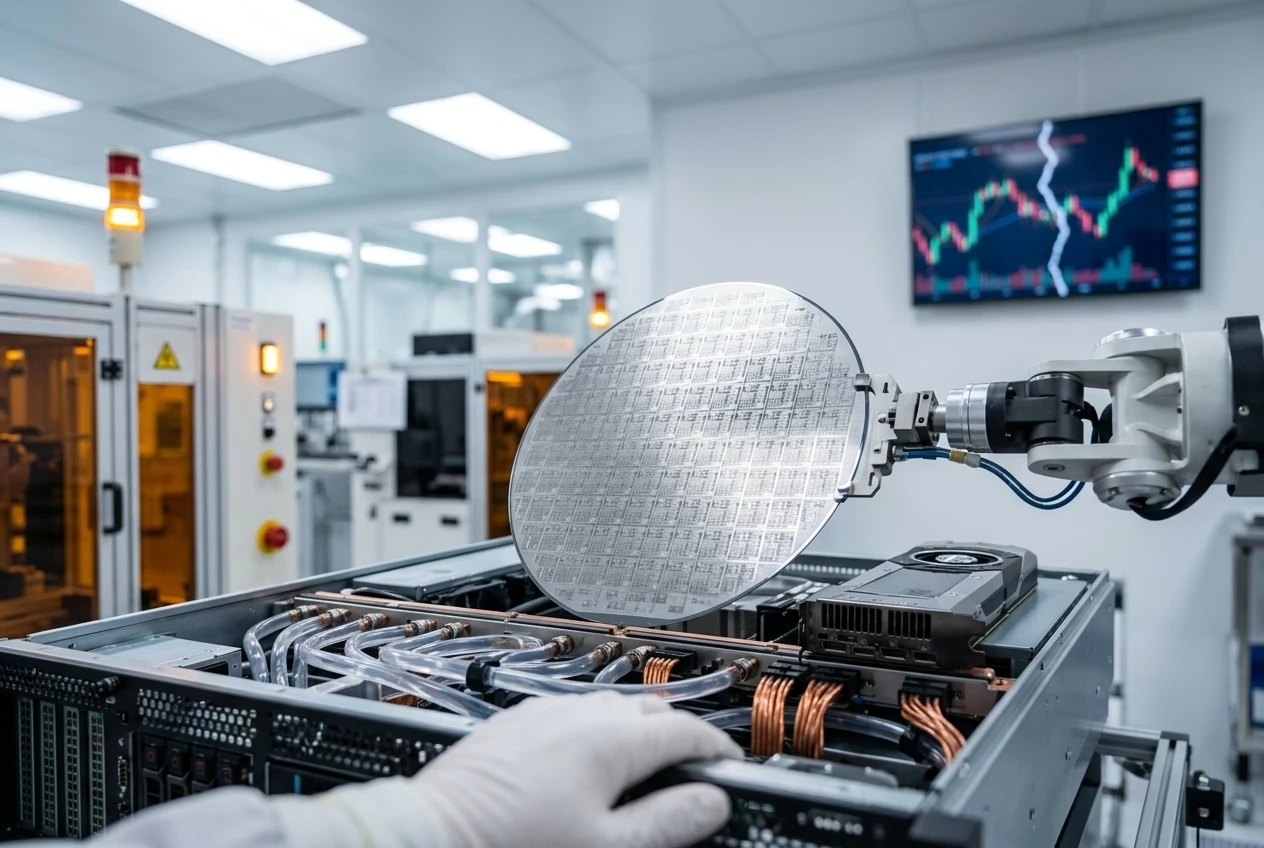

Flex is scaling Cerebras CS-3 production sevenfold in Milpitas as analysts split on whether the AI infrastructure stock is cheap or overpriced.

Flex Ltd., the Austin, Texas-based electronics contract manufacturer, has agreed to boost production of Cerebras Systems’ CS-3 AI supercomputer sevenfold by the end of 2026, expanding its Milpitas, California, plant to keep pace with demand. Shares of Flex (NASDAQ: FLEX) jumped 7.8% the day the deal became public. A month later, they are down 13.74%.

That gap between the pop and the pullback sits at the center of a bigger argument. At $128.72 a share, Flex looks cheap by one measure and expensive by another, and the business generating most of this AI enthusiasm is scheduled to become a separate company within months.

Seven Times the Cerebras Capacity by Year’s End

Flex and Cerebras Systems, one of Nvidia’s most closely watched AI chip challengers, announced the expanded manufacturing partnership on July 9, 2026, aiming to scale production of the CS-3 AI accelerator system at Flex’s Milpitas facilities.

The expansion is expected to lift CS-3 production capacity by roughly seven times through the end of 2026. Flex is adding new assembly and integration lines, more floor space, upgraded test infrastructure and additional manufacturing staff to get there.

The CS-3 runs on Cerebras’ wafer-scale engine, a single chip described by the companies as physically larger than any conventional AI processor. Building one requires liquid cooling, high-density power delivery, precision mechanical assembly and dense networking gear, backed by advanced test infrastructure and added manufacturing talent in California.

The CS-3 is unlike any computer system ever built, and scaling its production requires an extraordinary manufacturing partner.

Dhiraj Mallick, chief operating officer at Cerebras Systems, said of the deal. Flex, he added, brings the technical depth and operational rigor needed to support that scale.

Both companies frame the expansion as evidence that sophisticated AI hardware does not have to be built overseas, with engineers and technicians across the U.S. now assembling frontier AI systems for customers worldwide.

The Rally Lasted Less Than a Week

Shares of Flex jumped 7.8% in the afternoon session after the Cerebras news broke, a bigger single-day move than most swings the stock has logged this year.

Cerebras, which trades separately under the ticker CBRS, rose even harder. The AI chip challenger popped roughly 10% the same day as traders cheered the manufacturing scale-up.

Flex is no stranger to big swings. The stock has had 30 moves greater than 5% over the past year. The Cerebras news landed in the middle of an already turbulent stretch: Flex joined the S&P 500 on June 22, 2026, and was removed from the Russell 2500 Index and Russell 2500 Value Benchmark that same month.

None of that momentum held. A month after the Cerebras announcement, Flex trades at $128.72, down 13.74% over that stretch even as the shares remain up 102.14% for the year. The stock touched a 52-week high of $161.94 in June.

Zoom out further and the run looks even bigger. Investors who put $1,000 into Flex five years ago would have $8,172 today, a reminder of how much ground the stock has covered even through this month’s pullback.

A Data Center Business Growing 38% a Year

Flex closed fiscal 2026, the year that ended in March, with $27.9 billion in net sales, up 8.14% from $25.81 billion the year before, and adjusted earnings per share of $3.30, a 25% increase year over year.

The Cloud and Power Infrastructure segment, the unit closest to the Cerebras work and the rest of Flex’s AI buildout, grew revenue 38% in fiscal 2026, beating the company’s own 35% target. Adjusted operating margin reached 6.3%, hitting a goal Flex had set for fiscal 2027 a year ahead of schedule.

| Metric | Fiscal 2026 (Actual) | Fiscal 2027 (Guidance) |

|---|---|---|

| Net sales | $27.9 billion | $32.3 billion to $33.8 billion |

| Adjusted EPS | $3.30 | $4.21 to $4.51 |

| Adjusted operating margin | 6.3% | Further improvement targeted |

| Cloud and Power Infrastructure growth | 38% | SpinCo targets 65% to 75% |

That guidance implies 18% revenue growth and 32% adjusted EPS growth at the midpoint for fiscal 2027, a sharp step up from the 8.14% Flex just posted.

The Spin-Off That Complicates the AI Trade

On May 5, 2026, Flex announced plans to split into two independent public companies. One will hold the Cloud and Power Infrastructure segment, the business most tied to AI data centers. The other will keep the Integrated Technology Solutions and Regulated Manufacturing Solutions segments, Flex’s broader contract manufacturing base.

The transaction is structured to be tax-free for shareholders, with completion targeted for the first quarter of calendar 2027.

Flex management called the split a ‘no-brainer’ on the fiscal fourth-quarter earnings call, citing a one-time shift in AI data center architecture that a focused, stand-alone company could chase more effectively.

Flex is spinning off its AI data center power unit into a company targeting 65% to 75% revenue growth in fiscal 2027 and more than 80% in fiscal 2028, while the remaining business aims for low to mid single digit growth and prioritizes cash generation.

Flex closed a $1.1 billion acquisition of Electrical Power Products after the fiscal year ended, adding utility-grade gear for grid modernization. A regulatory filing shows Flex returned $944 million to shareholders through buybacks in fiscal 2026.

Flex has also been trimming. Chase Corporation agreed to acquire Sheldahl, Flex’s specialty coated films and flexible circuit business, part of a broader portfolio cleanup that has paired the AI buildout with divestitures elsewhere.

Is Flex Stock Still Undervalued?

By one popular yardstick, yes. A widely followed discounted cash flow model puts Flex’s fair value at $160.40, about 19.8% above the $128.72 share price. By a simpler measure, the stock’s price to earnings ratio of 53.6 times is nearly double the broader electronics industry’s 30.8 times, which is why the answer changes depending on which tool an investor trusts.

The bull case leans on Flex’s own numbers. The most followed valuation narrative points to 35% forecast annual growth in the data center segment as the reason revenue and margins keep expanding, with the Cerebras ramp folded in as fresh evidence for that thesis.

| Valuation Approach | Verdict | Key Figure |

|---|---|---|

| Discounted cash flow narrative | Undervalued | Fair value $160.40 vs. $128.72 share price |

| Price to earnings vs. industry | Expensive | 53.6x vs. 30.8x industry average |

| Price to earnings vs. fair ratio | Room to re-rate | 53.6x actual vs. 66x fair ratio |

| GuruFocus GF Value | Significantly overvalued | GF Value $43.18 vs. $155.81 late-June price |

Analysts mostly side with the cheap case. The average 12-month price target sits at $160.40, up from $81.44, with a Strong Buy consensus across 11 analysts. Barclays has gone further, raising its target to $203 from $174 while keeping an Overweight rating. Not everyone agrees: Freedom Capital Markets initiated coverage with a Hold, arguing the stock already looks overvalued at its current multiple.

On a forward basis, using next year’s expected earnings, the multiple eases to 30.14 times, and the PEG ratio, which weighs price against expected growth, sits at 0.66, a level growth investors typically read as inexpensive.

Hyperscalers Hold the Leverage

Strip away the valuation debate and the operating risk is straightforward. Flex’s AI data center business depends on a small number of hyperscale customers. If a major one pulls work in house or slows orders, the effect would show up fast, given how much of Flex’s recent growth rides on a handful of relationships.

- Customer concentration – a handful of hyperscale and large data center clients account for an outsized share of AI-related revenue, giving them significant pricing power.

- Thin contract manufacturing margins – an adjusted operating margin of 6.3% leaves little cushion if input costs rise or a customer renegotiates.

- Spin-off execution risk – separating the Cloud and Power Infrastructure unit into a stand-alone company by early 2027 involves new reporting lines, contracts and capital structures still being worked out.

- Valuation risk – a Strong Buy consensus and a $160.40 average price target already assume AI infrastructure growth continues at close to its current pace.

Flex reports fiscal first-quarter 2027 results on July 29, 2026, the next scheduled test of whether the Cerebras ramp and the rest of the AI infrastructure business are growing fast enough to justify the price investors are already paying.

Frequently Asked Questions

What Is the Cerebras CS-3 That Flex Is Manufacturing?

The CS-3 is Cerebras Systems’ wafer-scale AI supercomputer, built around a single chip physically larger than any conventional AI processor. It bundles liquid cooling, high-density power delivery and networking gear into one system designed for large-scale AI training and inference workloads.

Is Flex Financially Stable Despite Its Rich Valuation?

Flex carries an Altman Z-Score of 2.58 and a Piotroski F-Score of 6, according to data from S&P Global Market Intelligence. A Z-score below 3 is typically read as a signal of elevated bankruptcy risk in the underlying academic model, though it is only one of many financial health indicators analysts weigh.

When Will Flex Complete Its Cloud and Power Infrastructure Spin-Off?

Flex is targeting the first quarter of calendar 2027 for the tax-free separation. Shareholders are expected to get more detail at Flex’s annual general meeting, scheduled for August 5, 2026.

How Big Is Flex’s Data Center and AI Infrastructure Business?

For fiscal 2026, Flex projected data center revenue of roughly $6.5 billion, about a quarter of total company revenue, with growth of at least 35% built into management’s own targets for the segment.

What Other AI Hardware Makers Does Flex Work With Besides Cerebras?

Flex has also expanded collaborations with NVIDIA and LG on data center and AI infrastructure hardware, part of a broader strategy to diversify its AI manufacturing customer base beyond any single partner.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Flex is a publicly traded stock, and the valuations, price targets and forecasts discussed here carry real uncertainty. Consult a licensed financial advisor before making investment decisions. Figures are accurate as of publication on July 16, 2026.

YouTube Joins Meta’s Appeal of the Social Media Addiction Verdict

Russian Realtors Could Soon Verify Credentials via Max Messenger

Apple’s Maps Ad Rules Quietly Dodge Google’s Messiest Ad Categories

Globe Telecom Backs Regulating Social Media Access for Under-16s

Argentina Inspects Pickford’s Water Bottle After Beating England Anyway

Eye Doctors Warn Childhood Myopia Is Rising Faster Than Ever

OnePlus to Exit India, US and Europe in OPPO’s Broader Retreat

Xero Shares Rebound to A$69.83 as CEO Pay Fight Overshadows Gains

OnePlus Faces a Deeper Retreat as India Joins Oppo’s 2027 Exit Plan

Bitcoin’s Quantum Threat Needs 500,000 Qubits, Not Today’s 105

Google Search Profiles Build a Follow Graph Inside Discover

Microsoft Xbox Layoffs Start in July as Sharma Slams 3% Margin

Oracle Cuts 21,000 Jobs in a Year, Cites AI in 10-K Filing

Moonshot AI Targets $30 Billion in China’s Fastest AI Funding Sprint

WhatsApp Meta Business Agent Reaches India, With a New Pricing Meter

XPL Rallies 30% Ahead of Plasma One Card Tier Launch

SpaceX’s Google Deal Turns a Rocket Company Into a Cloud Landlord

Oppo’s ColorOS 17 Eligibility List Leaves A-Series Buyers Behind

Google DeepMind and A24 Sign $75 Million AI Partnership Deal

Meta’s Iris AI Chip Enters Production in September, Tests Clean

-

NEWS1 month ago

NEWS1 month agoGoogle Search Profiles Build a Follow Graph Inside Discover

-

GAMING1 month ago

GAMING1 month agoMicrosoft Xbox Layoffs Start in July as Sharma Slams 3% Margin

-

AI3 weeks ago

AI3 weeks agoOracle Cuts 21,000 Jobs in a Year, Cites AI in 10-K Filing

-

AI1 month ago

AI1 month agoMoonshot AI Targets $30 Billion in China’s Fastest AI Funding Sprint

-

AI6 days ago

AI6 days agoWhatsApp Meta Business Agent Reaches India, With a New Pricing Meter

-

CRYPTO1 month ago

CRYPTO1 month agoXPL Rallies 30% Ahead of Plasma One Card Tier Launch

-

AI1 month ago

AI1 month agoSpaceX’s Google Deal Turns a Rocket Company Into a Cloud Landlord

-

NEWS1 month ago

NEWS1 month agoOppo’s ColorOS 17 Eligibility List Leaves A-Series Buyers Behind