COMPUTERS

HDD Head Manufacturing Is the New AI Storage Chokepoint

Seagate’s hard disk drive head manufacturing expansion in Bloomington signals AI storage demand outrunning industry constraints, with unit growth projected at 1.2%.

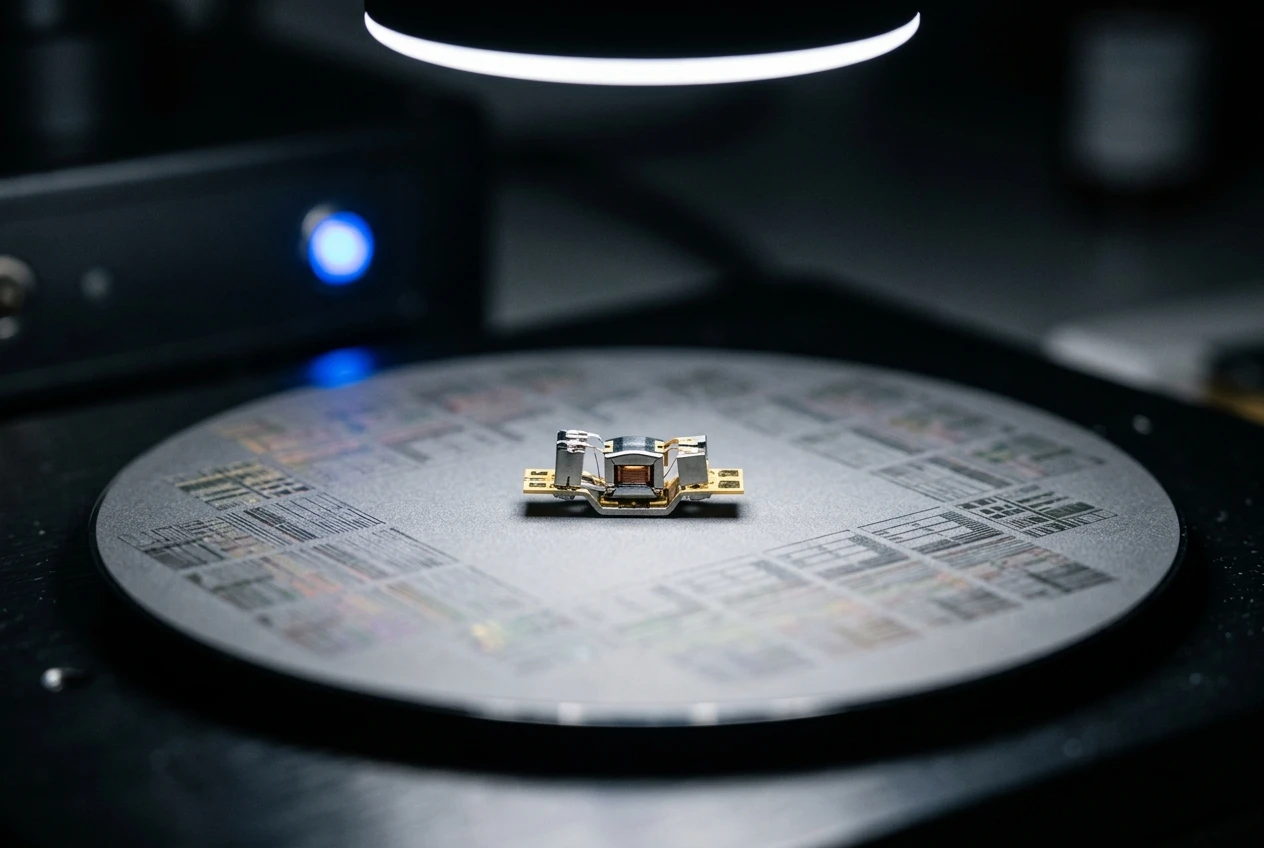

Seagate is pouring 19,000 square feet of new clean-room space into its Bloomington, Minnesota plant, nearly tripling the existing 11,000 square feet used for hard disk drive head manufacturing. The new space is dedicated to wafer production for the magnetic recording heads that cap how many drives the industry can build each quarter. Head manufacturing has been the gating factor in HDD production for years, and AI-driven storage demand is forcing a faster scale-up than the industry has attempted in a long time.

Coughlin Associates projects HDD unit shipments will grow 1.2% from 2025 to 2026, with a median 11% gain through 2030. The unit numbers are modest next to the 34% jump in total capacity shipments forecast for 2025. The build-out of head plants at Seagate and TDK points to a faster scenario, with up to 30% unit growth by 2030 in the high case. Each of those outcomes depends on the same constraint: how many heads can be produced each quarter.

Bloomington Is the New HDD Chokepoint

Hard disk drives look like simple aluminum boxes, but their throughput is set by one component: the magnetic recording head. Heads ride on a cushion of air a few nanometers above a spinning platter, manufactured on ceramic wafers with processes borrowed from semiconductor fabrication. Seagate’s Bloomington plant is its recording head development and manufacturing arm, with TDK as the other major external supplier for Toshiba and at times for Seagate and Western Digital.

Seagate’s plan to add 19,000 square feet of clean room almost triples the 11,000 square feet already there, bringing the wafer-fab footprint to roughly 30,000. The company told Bloomington planning officials, in the Bloomington factory expansion plans reported by the Minnesota Star Tribune, the extra space would significantly increase semiconductor wafer fabrication capacity, with construction leaving room on the west side of the campus for another expansion if needed.

Levi Nelson, Seagate’s facilities project manager, said the new space will produce hard-drive recording heads, including newer magnetic technologies. The shift is happening as Seagate expands HAMR head output, and the rest of the industry is preparing to follow. WD has indicated it will buy HAMR heads from TDK if it cannot ramp its own program fast enough, and Toshiba is widely expected to do the same.

- Seagate: In-house head manufacturing at Bloomington; HAMR heads being added to capacity

- Western Digital: In-house head development, with TDK as backup supplier

- Toshiba: TDK is the primary head supplier

- Industry-wide: TDK and Resonac (formerly Showa Denko) are the only qualified HAMR media suppliers

The Unit Shipment Forecast Is Modest, but Real

Tom Coughlin, president of Coughlin Associates, has been tracking HDD shipments for decades. His latest numbers show that the long decline in HDD units, set off by the rise of solid-state drives, has finally flattened. The 2025 total landed near 124 million units, the same as 2024, and 2026 looks slightly higher.

Capacity is moving much faster than unit counts. The 2025 storage capacity total is estimated at 1.79 zettabytes, a 34% jump from 2024, and Coughlin projects 6.5 zettabytes by 2030. The gap reflects platters and heads getting bigger, with the average shipped drive capacity climbing rather than unit volumes. The growth in dollars-per-terabyte terms keeps getting more favorable for HDDs even as the unit count stays flat.

The mix of HDDs is also shifting toward nearline drives, the high-capacity models used in data centers. Coughlin estimates nearline units were 67% of all HDDs shipped in 2025, up from 57% in 2024, and projects nearline will be over 90% of the total by 2030.

AI is the demand driver. HDDs are cost-effective secondary storage for AI model logs, training data, and other long-tail content, and the three drive makers have long-term contracts with major data centers running out to 2027. The latest reading on contract pricing shows HDD prices jumped roughly 4% quarter over quarter in the fourth quarter of 2025, the kind of move that signals demand outrunning the supply of drives.

- 2025 unit shipments: ~124 million (Coughlin estimate)

- 2026 unit growth over 2025: 1.2%

- 2026-2030 median growth: 11%

- 2026-2030 high case: 30% (if head plants expand on schedule)

- 2025 capacity growth over 2024: 34%, to ~1.79 zettabytes

Why the Drive Makers Stopped Reporting Units

Since the third quarter of 2025, both Seagate and Western Digital have made it harder to find out how many HDDs they ship each quarter. The two companies have moved to reporting total HDD storage capacity, in zettabytes, and stopped giving a unit count alongside it. Coughlin warned that the change would leave investors with additional risk, since they would not know actual product production information. The shift was buried in routine quarterly reporting, and the consequence is that the public now knows more about how much storage shipped than about how many drives carried it.

The change is partly about emphasis and partly about what’s selling. Both Seagate and Western Digital say they are focused on capacity contracts rather than unit volumes. Western Digital has increased disks and heads per drive up to 11, with plans for 14, while Seagate has stayed at 10.

The 100TB HAMR Roadmap

Western Digital used its February 2026 Innovation Day to lay out a hard drive roadmap built around two parallel tracks: an ePMR line that extends to higher capacities, and a HAMR line that scales further. The two run on a common platform that lets customers drop either drive into the same chassis, with WD saying the highest-capacity ePMR drive is in qualification at two hyperscale customers and HAMR drives ramping at two more in 2027. The capacity targets differ by maker, and the table below summarizes where each is heading.

The capacity gains come from more platters and a higher-density recording technology. WD is using an 11-platter platform for its first commercial HAMR drives, with edge-emitting lasers heating iron-platinum media to a specific temperature, and is detailing a 14-platter platform that, paired with 10 terabytes per platter, points to drives well into the 100TB range by the end of the decade. The vertical-emitting laser WD is developing is built using lithography that allows wafer-level testing, a fix for the low yields of the current design.

By emitting more light, harnessing more of that light into the recording technology, we will increase the aerial density of the HAMR platters from four terabytes all the way to 10 terabytes by 2028 per platter.

Ahmed Shihab, chief product officer at Western Digital, said it at the company’s Innovation Day 2026, in a deep-dive on WD’s 14-platter HAMR designs.

Seagate is ahead on HAMR volumes. The company said it had shipped over 1 million HAMR units in 32TB and 36TB capacities out of an estimated 12.5 million total drives in its most recent quarter, with the lab demonstrating 6.9 terabytes per disk and the product maturity chart pointing to 40-plus-terabyte drives in 2026, 50-plus-terabyte drives by 2028, and 100TB drives possible by the early 2030s. The catch is the same constraint that defines the whole industry: the heads required for higher capacities take longer to qualify and produce than the platters they read.

| Maker | 2026-2027 target | 2028-2029 target |

|---|---|---|

| Western Digital | 40TB UltraSMR ePMR; HAMR ramp 2027 | 60TB ePMR; 100TB HAMR by 2029 |

| Seagate | 40+TB HAMR volume | 50+TB HAMR |

| Toshiba | 12-disk 2026; 30+TB HAMR | Not announced |

Sources: WD’s Innovation Day 2026 announcement; Coughlin Associates 2026 projections, summarized in Coughlin’s full 2026 storage projections.

HDDs Sit in the Middle of the AI Storage Stack

AI training and inference generate a lot of data, and the cheapest place to keep it is on a hard drive. Coughlin estimated the average shipping HDD capacity will increase by about 2.7 times between 2025 and 2030, and the gap between HDD and SSD cost per terabyte is likely to stay greater than 4X out to 2030. The result is that HDDs end up holding the long tail, with higher-capacity QLC NAND flash drives picking up the active data and HDDs absorbing the rest.

Hyperscale data center operators are buying everything the drive makers can ship, and the supply is locked up. Long-term contracts between the three drive makers and major data centers run out to 2027, and nearline drives are in short supply in 2025, a fact that has lifted average selling prices alongside the unit count. The current ASP trend is up, in contrast to the long-term HDD price decline, and the flip is being driven entirely by the nearline-heavy mix.

The new design tier is one that closes the bandwidth gap between disk and flash. WD’s High Bandwidth Drive technology and Dual Pivot actuator are designed to push HDD bandwidth from 2X to 8X, which the company says can let drives match QLC SSD bandwidth on AI workloads. Power-optimized HDDs in qualification at WD in 2027 are aimed at the warm-data tier, sitting between current nearline drives and tape.

The storage stack is shaping up as a four-tier hierarchy. HBM sits on the AI accelerator itself; NAND flash, including the new High Bandwidth Flash tier that Sandisk is pushing, handles the hot data; HDDs take the warm-to-cold long tail; tape holds the archive.

What the Head Expansion Means

Seagate’s Bloomington build, plus TDK’s earlier expansion of suspension and head production, are the supply-side answers to a demand question the HDD industry didn’t expect to be answering a few years ago. The unit shipment range Coughlin projects for 2030, 11% median and 30% in the high case, depends on those head plants coming online on schedule. Both companies have said the new capacity arrives 12 to 18 months after breaking ground, putting the earliest of the new head output in late 2027 or 2028.

The biggest open question is what AI capex looks like in 2026 and 2027, which determines whether the high case is the one that plays out. Google’s $15B Vizag AI infrastructure push is one of the larger single commitments announced so far, and the AI infrastructure footprint is now measured in hundreds of billions of dollars across the hyperscalers. For now, the public is reading the industry through capacity-only reporting, with the 1.2% unit growth estimate a best guess rather than a number anyone can verify. Coughlin’s next HDD shipment reading will land later in 2026, when the first 40TB drives qualify at hyperscalers and HAMR volumes start to register on the balance sheet.

Frequently Asked Questions

Why are hard disk drives still being made in 2026?

HDDs cost a fraction of what SSDs cost per terabyte, and the gap is expected to stay above 4X out to 2030. AI workloads generate petabytes of data that don’t need flash-tier latency, and the three HDD makers have multi-year contracts with hyperscale data centers running into 2027. Tape is colder and more archival; HDDs hold the long tail of model logs, training data, and other secondary content that has to stay accessible.

What is HAMR and why does it matter for AI?

HAMR stands for heat-assisted magnetic recording. A small laser on the recording head heats a tiny spot on the platter just before it is written, allowing much denser magnetic storage. Seagate has shipped over 1 million HAMR drives to date, and WD is qualifying HAMR drives at two hyperscale customers with production planned for 2027. The technology is the path to 100TB drives and beyond, and is the reason head manufacturing is now the gating factor for the whole industry.

Why are HDD prices going up?

Hyperscalers are buying every drive the makers can build, and the supply is locked into long-term contracts running out to 2027. Coughlin noted that contract prices jumped roughly 4% quarter over quarter in the fourth quarter of 2025, with nearline drives in short supply for the year. Higher per-drive capacity (more disks, more heads) and a nearline-heavy mix have also pushed the average selling price up since 2015.

What does it mean that drive makers stopped reporting unit shipments?

Both Seagate and Western Digital have moved to reporting only capacity (in zettabytes) since the third quarter of 2025, ending the practice of disclosing unit counts alongside revenue. Coughlin and other analysts warn this leaves investors with less visibility into actual product production, since capacity tells you how many terabytes shipped but not how many boxes shipped. For 2025, third-party estimates put unit shipments at roughly 124 million, the same as 2024 and well below the 2010 peak.

Will HDDs be replaced by SSDs?

Not in the foreseeable future for bulk storage. The cost gap is too wide, the AI capacity demand too large, and the technology roadmap too long to allow flash to displace disks in the data center. WD’s plan to push HDD bandwidth from 2X to 8X, plus a power-optimized tier between warm and cold storage, is aimed at closing the use-case gap with flash on AI workloads. The result is layering rather than replacement.

CAA Demands Meta Default Muse Image to Opt-In Consent

Memory Costs Are Quietly Squeezing Low-End Phones and PA Suppliers

Social Media Algorithms Now Reward Watch Time, Not Conversation

ResMed Cuts a $490 Million Deal to Exit MatrixCare Software

Nothing’s Phone (4b) Lands at £299, Just £50 Below the Better 4a

Parents’ Phone Distraction Tied to Teen Insecure Attachment

AirPods Custom EQ and Adaptive Audio Slider Arrive in iOS 27 (9A5314b)

EU Court Rejects Apple’s Three Challenges to Its Gatekeeper Status

Black Flag Resynced Playable Build Leaks Ahead of July 9 Launch

Penton Publications Enters Liquidation on 3 July 2026

Microsoft Xbox Layoffs Start in July as Sharma Slams 3% Margin

Google Search Profiles Build a Follow Graph Inside Discover

Google DeepMind and A24 Sign $75 Million AI Partnership Deal

DGO App Brings Rs 549 Mobile Pass for FIFA World Cup 2026 in Nepal

Oracle Cuts 21,000 Jobs in a Year, Cites AI in 10-K Filing

Oppo’s ColorOS 17 Eligibility List Leaves A-Series Buyers Behind

Anthropic Tells Senators Alibaba Ran the Largest Claude Distillation Attack

Apple Strikes Preliminary Deal For Intel To Make iPhone And Mac Chips

Andreessen Horowitz Bets $2.2B on Crypto’s Quiet Cycle

Google Home Spring Update Adds Gemini 3.1 And Old Nest Cam AI

-

GAMING4 weeks ago

GAMING4 weeks agoMicrosoft Xbox Layoffs Start in July as Sharma Slams 3% Margin

-

NEWS1 month ago

NEWS1 month agoGoogle Search Profiles Build a Follow Graph Inside Discover

-

AI2 weeks ago

AI2 weeks agoGoogle DeepMind and A24 Sign $75 Million AI Partnership Deal

-

APPS4 weeks ago

APPS4 weeks agoDGO App Brings Rs 549 Mobile Pass for FIFA World Cup 2026 in Nepal

-

AI2 weeks ago

AI2 weeks agoOracle Cuts 21,000 Jobs in a Year, Cites AI in 10-K Filing

-

NEWS1 month ago

NEWS1 month agoOppo’s ColorOS 17 Eligibility List Leaves A-Series Buyers Behind

-

AI2 weeks ago

AI2 weeks agoAnthropic Tells Senators Alibaba Ran the Largest Claude Distillation Attack

-

NEWS2 months ago

NEWS2 months agoApple Strikes Preliminary Deal For Intel To Make iPhone And Mac Chips